Shubham Dharmsktu, a 26 years old young explorer of Uttarakhand walked from Kashmir to Kanaya Kumari by foot in 2018 hoping to shed light on India’s waste management scenario. Kashmir to Kanaya Kumari is a distance of 2,856 kms approx. It represents the distance which starts from Kashmir and ends with Kanaya kumari.

Generally to measure the distance there should be the beginning as well as the end. In the same way, in accounting also one should know where accounting starts and where it ends.

Entrepreneurs, who commence their business, they might be aware of certain accounting norms or accounting procedures. But many are not aware of the use/purpose of accounting. Often entrepreneurs are more concerned about the profit of the organization, but no one knows the profit of the business also depends on the better understanding of the accounting.

For this, one must know where accounting starts & where it ends…!

In this article we are going to discuss on the topic Accounting Cycle and the table of contents (i.e. Basket of Mangoes) are given below for quick navigation.

Basket of Mangoes

What is Accounting Cycle:

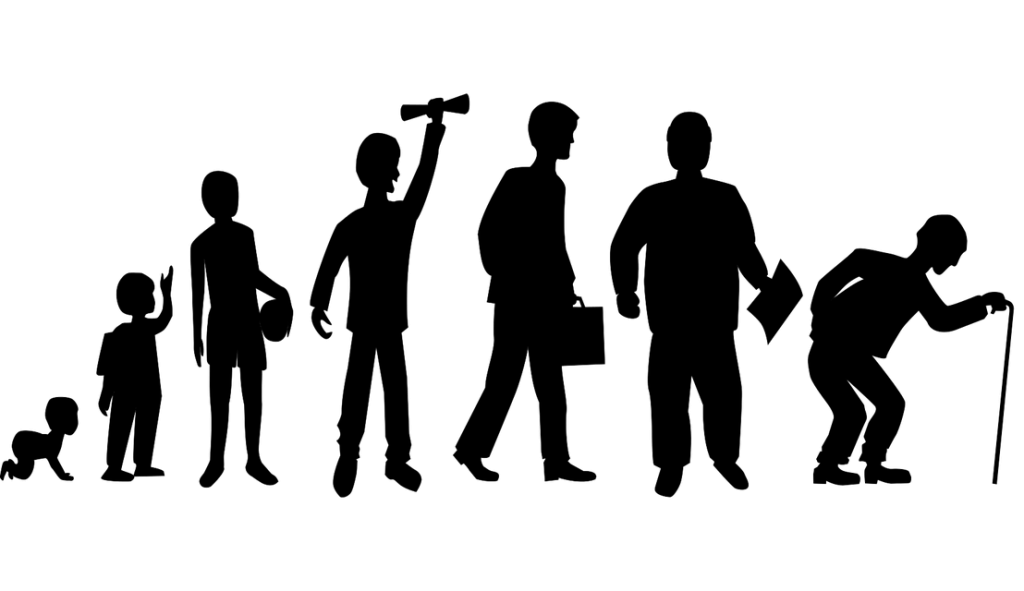

Do you know Human life cycle..!!

Accounting Cycle can be better understood with Human Life Cycle. As human life passes through multiple phases before it ends at one phase, similarly accounting cycle also contains multiple phases which describes the complete sequence of accounting from the beginning to till the end.

Accounting Cycle is a complete cycle of accounting, which ranges from identification of financial transactions to preparation of Final accounts.

Steps for Accounting Cycle

In Accounting Cycle, there are several steps to understand through which you can gain complete knowledge on Accounting. Now, we will discuss what exactly accounting cycle contains and understand in detail about the each step involved.

1. Identification of Transactions

Will you remember every person that you come across in your daily routine?

No!!!

Why..?

Because it is not necessary to remember each and every person that you meet and it is not practically possible also. But we will obviously remember the persons with whom we interact more. Similarly, in the accounting also we don’t record all the transactions of business. Our primary task is to identify the transactions which are to be recorded.

Only financial transactions (i.e. transactions which can be expressed in money terms) are to be recorded in the books of accounts. For example, Mrs. Jyoti made an agreement to sell Kashmir Apples for Rs.5,00,000 to a dealer of Andhra Pradesh.

Whether it is a transaction?

Will we record this transaction in the books of accounts..!!

No..!!

Why?

The above agreement is a transaction. However it cannot be called as financial transaction because, there is only agreement made between the parties. But the actual transaction which we can express in the monetary terms did not happen between the parties. So this transaction need not be entered in the books of accounts.

Hence, before entering any transaction in the books of accounts we need to identify whether it is a financial transaction or not. If it is a financial transaction we need to enter those transactions in the books, otherwise need not.

2. Book Keeping

Book keeping is the process of recording the financial transactions of a business. These include transactions relating to purchases, sales, receipts and payments. Any person who is responsible for recording these financial transactions in the books of accounts is known as “Book Keeper“.

Though the prominent method of book keeping is double entry system, there are several other methods also available for book keeping process.

After identifying the transactions, next step is to classify them into financial and non-financial transactions. As mentioned above, we are concerned about the financial transactions only.

We shall enter those transactions in the books of accounts which is the preliminary stage of accounting. In this stage, we record the transactions in a set of records which can be also called as “Preliminary records“.

Also read this: 8 Differences between Book keeping and Accounting

3. Recording of Transactions

As soon as a transaction happens (of course, it should be financial transaction) in a business, it shall be recorded in the books of accounts.

In olden days, this process of recording the transactions was done by maintaining different set of physical books. Now a days, with the introduction of technology recording of transactions became very easy. In the market, there are multiple software options available for maintaining the records electronically, of which the prominent packages are Tally ERP 9 & Quick books etc. If you are able to record the journal entry properly, then automatically these softwares will prepare the ledgers, Trial Balance & even Final accounts too.

Example:

1. Mr. Subba Rao, who is a cashier purchased goods worth of Rs.8,000. There are two aspects of the transaction. One is Purchases and the other one is cash. Thus, It should be recorded in the Purchase register (i.e. one of the subsidiary books) & Cash book (In case of Cash purchases). In case of Credit purchase, the same will be entered in the “Purchase register” and “Creditors/Supplier’s Register”.

Now, we understood the impact of the transaction. Let’s also understand how to write/pass the Journal entries as per the Golden Rules of Accounting.

Also read this: Golden Rules of Accounting – An Easy Understanding

4. Journal

What is a Journal…?

& What transactions will be entered in the Journals….?

A Journal records all the financial transactions of a business. All these transactions are to be recorded in a chronological way. Every transaction recorded in a journal is also supported by a narration which explains the nature of such transaction. However, while passing these entries one must ensure that both the Debit and Credit sides matches.

Let’s understand with the help of examples:

Example 1:

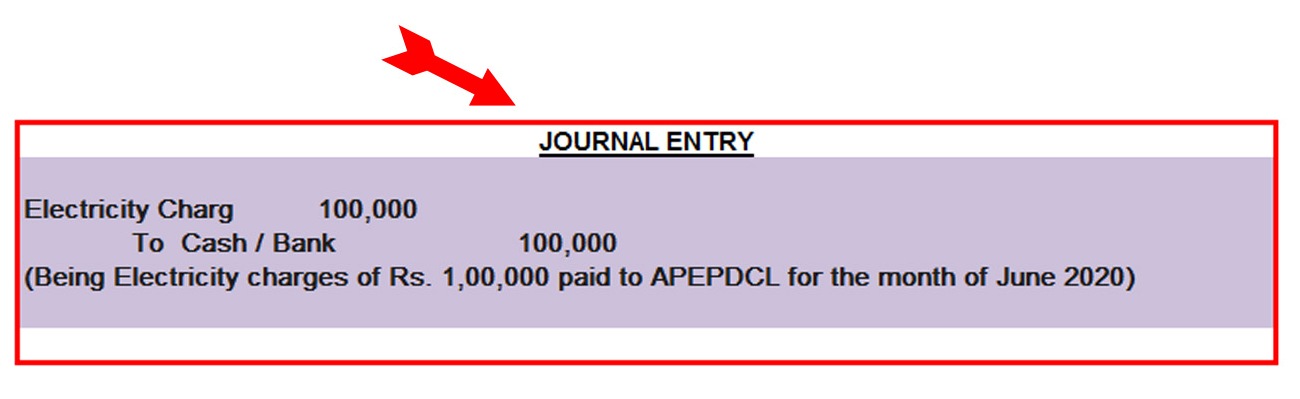

M/s. Sonakshi Ltd paid Electricity charges of Rs.1,00,000 to APEPDCL for the month of June 2020.

Entry for the above transaction will be:

The description mentioned in the brackets is “Narration”, which describes the nature of the transaction.

Example 2:

2. M/s Himaja Ltd received a Quotation for purchase of Water Purifier of Rs.10,000.

It is not a financial transaction since there is no monetary element involved. Hence no need to record the transaction in books of accounts.

Now, Let’s jump into next step of Accounting Cycle of Ledger.

5. Ledger

Generally in every organization there will be numerous entries in a financial year. Out of which, identifying

(i) how much was spent towards a particular expenditure or

(ii) how much was generated from a particular source of income

is almost impossible.

Suppose, you want to identify how much is spent for purchases in a particular month. So the only way for identification is “look for all purchases accounted in the journal and sum it”.

Looks easy, isn’t it?

But certainly not.

However we can give a try for organizations with minimal transactions, but adopting the same for large organizations is certainly not a wise move. Moreover, It is hectic and time-consuming process.

So what is the alternative method of doing it?

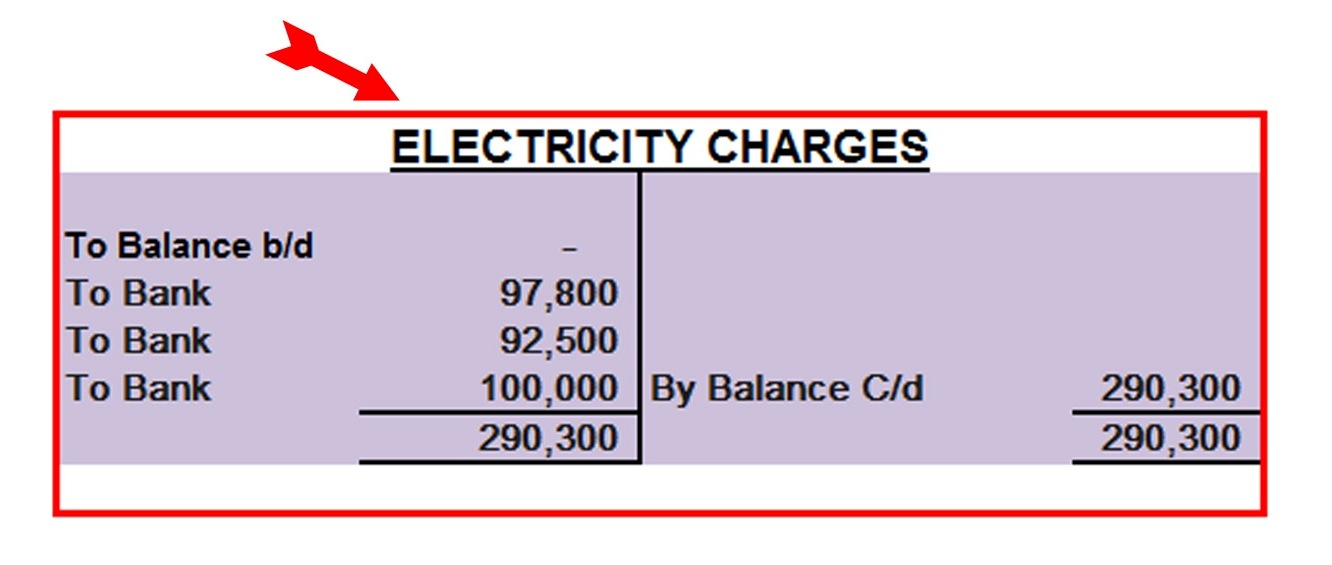

It is known as “Ledger”. Ledger will play a key role in identifying all the transactions at one place, which are done by any entity in a particular period. These are represented by “T” form structure which can be observed below:

Ledger basically gives you all the details of the transactions related to asset, liability, expense & income in a particular period. Indirectly it helps in quick decision making. In olden days, these ledgers were maintained manually with the help of journal entries. But thanks to the technological advancements done in the accounting also, which makes it very easy. Now if you are able to pass the journal entries, these accounting softwares (i.e. Tally & Quickbooks etc.) will prepare ledgers, Trial Balance and Final accounts automatically.

So, the basic difference between the Journal & Ledger is

Journal is related to a transaction, where as Ledger is group of related transactions.

6. Trial Balance:

Life is all about to make the right balance which keeps you strong in tough times.

Trial balance is a statement which represents the balances of all ledgers at one place. It is prepared to ensure that all the debit and credit aspects of the transactions, on any particular day are matching with each other.

Generally, Trial Balance is prepared at the end of each financial year before the preparation of final accounts. As the books of accounts are maintained on double entry basis, debits and credits should match to proceed for the preparation of Profit & Loss account and Balance Sheet.

7. Adjustment Entries:

What are the adjustment entries…?

Whether the adjustment entries needs to be shown in the books.

Of course, Yes..!!

In a normal phenomena, Life will have a lot of adjustments.

It’s all about how we improve ourselves in every stage.

Likewise in Accounting also, adjustment entries may be necessary to rectify the previously recorded transactions. And such adjustments are to be done as per applicable accounting principles.

For example, You might have returned the goods purchased for Rs.1,00,000 due to any damage or defect or improper quality. In such a case, Journal entry to be recorded in the books will be as follows:

Journal Entry is as follows

Return Outward a/c Dr 1,00,000

To Purchases a/c 1,00,000

If you observe the above entry, we have reduced the value of purchases by crediting it (normally purchase account will have debit balance) and Return outward (i.e. purchase returns) account is debited to record the goods returned.

Before preparing Financial Statements, one must record/consider and account for all the adjustment entries properly. Otherwise, the financials of the organization does not show True and Fair view of the transactions

8. Adjusted Trial Balance

An enterprise supplied goods worth Rs.1,00,000 to its customers. Customers after receipt of goods they found that Rs.15,000 worth of goods detreated /damaged. Now what will happen the in the Books of Seller. The Seller shall reduced his Sales in his books by Rs.15,000 as a Sales return. This is called an Adjustment entry.

The businesses after passing the necessary adjustment entries in the books of accounts, an adjusted Trial Balance has to be prepared, to check the arithmetical accuracy. With the help of such adjusted Trial Balance, we can prepare Profit and Loss account, Balance sheet and Cash flow statement effectively.

9. Closing Entries

Closing entry is an entry which will be made at the End of the Financial Year. The normal closing year for the assessee is 31st March of the every financial year. These closing entries will be made only for the Nominal Accounts only. All these nominal accounts shall be closed by transferring to trading account & profit and loss a/c.

For example, M/s X & Co purchased a Machinery on 01st Oct, 2020 worth of Rs.10 Lakhs which will be treated as an asset to X & Co. For X & Co Ltd the Financial year is 2020-21. Therefore, the normal closing year can be considered as 31st Mar,2021. At the end of the financial year of 31st Mar,2021, X Ltd shall calculate Depreciation as the Machine is used for 6 months for the business. In this case to close the books of accounts, X Ltd shall pass a Depreciation entry. The entry will be as follows.

Depreciation a/c Dr

To Machinery

Also read: CA Students: Freedom fighters of Life

10. Financial Statements

To assess the financial performance of any entity, we need to interpret their financial statements properly. Financial statements gives lot of insights about the performance of an entity, which is the basis for the top management to take relevant decisions effectively.

Preparation of Financial statements can be considered as an end to the Accounting Cycle. Financial Statements can be prepared easily which shows the true & Fair view of the financial position and operating results of the business.

The financial statements includes:

- Profit and Loss account (To ascertain Profit or Loss)

- Balance Sheet (To know What a Business Owns i.e. Assets & What a business Owes i.e. Liabilities)

- Cash Flow Statements (To ascertain total Inflow and Outflow of funds)

- Notes to accounts (Interpretation for the items considered in the accounts)

All the above statements will be prepared in case of profit oriented organizations. Where as in case of Non-Profit Organizations, nomenclature is slightly different even though the preparation and nature is more or less similar. Those are:

- Receipts and Payments accounts (Similar to Cash Book)

- Income and Expenditure account (Similar to Profit and Loss account)

- Balance Sheet

After preparing the financials, next step is to proceed for the audit of books accounts.

This is how an accounting process starts with recording the financial transactions and ends with the preparation of final accounts. As mentioned earlier in the article, if you are able to record the journal entries properly then the accounting software will do the balance for you i.e. preparation of ledgers, Trial balance & Final accounts. So make sure you start well to finish it off well.

I hope you understood the “Accounting Cycle” concept.

Please COMMENT which of the above topic you like the most. Also share this article to your Friends & Family

Thanks for reading..!!!

Disclaimer: Every effort has been made to avoid errors or omissions in this material. In spite of this, errors may creep in. Any mistake, error or discrepancy noted may be brought to our notice which shall be taken care of in the next edition. In no event the author or the website shall be liable for any direct, indirect, special or incidental damage resulting from or arising out of or in connection with the use of this information.